"Davos Man" is a neologism referring to the global elite of wealthy (predominantly) men, whose members view themselves as completely "international". I think it is a good thing that this definition has evolved over the past 50 years of this conference being held. There are a few drawbacks to this forum which this quote highlights well:  Niall Ferguson. Senior Fellow, Hoover Institution on Cognitive Dissonance. "There is a cognitive dissonance at the heart of Davos. Publicly, you have to agree with Greta Thunberg and be part of the virtue signaling community on climate change. But privately, you're all agreeing with Trump. You can't be outwardly too supportive. The reality is, is that if Europe cannot get some sustained economic growth, the Green Deal is just going to amount as another drag on German manufacturing and on the Euro zone as a whole. I think privately a lot of people were listening to POTUS and thinking 'you know what? He's actually been doing the stuff we should be doing: fiscal stimulus.' Everyone says the German's should do it. The U.S. has done it. They're probably thinking 'we should have some of that.'" Mr. Ferguson was just one of many global political and business leaders to join the CNBC's Squawk Box team in Davos over this past week. For the record, I watch more television this week than I do the entire year, to be certain. Cognitive dissonance aside, these individuals represent a slew of successful and influential men and women. I always find this week incredibly interesting as they all descend on a small town in Switzerland as "Masters of the Universe." It is important to highlight, the majority of the perspectives below are from CEO's who represent public companies and therefore have shareholders. They ALL have stakeholders and BOD's. When expressing their views, they are not expressing them as private citizens. Their voice represents the view of, most of the time, the highest ranking member in their respective company. What they say can move markets. It can move their share price. They have a responsibility to not be dishonest in their views, but possibly pander a bit to what is expected they say. Here are some snippets...  Mike Corbat. CEO, Citi on Fiscal Policy. "One of the things that has happened (globally) is we have become very reliant on monetary policy...in terms of entitlement reform and creating sustainability. The challenge when you get to where we are with low rates, or negative, is governmental balance sheets being called into question, and a lack of the creation of fiscal sustainability- it creates vulnerabilities. Part of the challenge of quantitative easing is that gap naturally widens. Those people that own assets, they increase. People that don't, have easy access to money."

Bill Ford. CEO, General Atlantic on Capital Discipline. *investors forcing companies to move more quickly towards profitability than growth.* "Capital discipline is back. 2018 and 2019, companies lost focus on business model, on capital utilization, on governance. What we are seeing now is the pendulum swinging back. How you use your capital matters. How you focus on your business model to reach profitability matters."

Stacey Cunningham. President, NYSE on IPO Markets Changing. "We shouldn’t categorize it as a bad year. It certainly was a good year. I think what we saw at the end of the year is investors start to ask questions that they hadn’t really been asking before, as we saw the difference between companies performing well when they had strong profits or a path to profitability and those that had more explaining to do as to how they were going to get there."  Larry Kudlow. National Economic Advisor to POTUS on Stakeholders. "I think any responsible company has to think about these things. You're talking about labor management relations, about community relations. I think that's a good thing. I don't think that should get in the way of profits and earnings because that is what drives the system. And judging from the stock market, the outlook there is still very good. We are opposed to a government-run, socialist economy. Beyond that, stakeholders are a good thing, it's just acting responsibly. But you can't forget the profit motive- that's what makes the whole thing run."

Scott Minerd. CIO, Guggenheim Partners on the Federal Reserve. "With the Fed pivot, we got a revival in economic activity, we've got the trade war on hold now. There are a lot of reasons to be positive on the economy. An old adage says 'expansions don't die of old age, the Federal Reserve kills them.' I would show them (NY Fed Reserve) how M2 growth is slowing down, and how they were being more restrictive than they realized. The quantitative tightening while the Fed was raising rates was a double whammy."

Paul Hudson. CEO, Sanofi on Drug Innovation. "It's an incredible moment for scientific innovation in general. Rare diseases, really debilitating life disorders. We have an opportunity to work with the FDA, which is why we are taking advantage of that. It's a great time for data transparency to speed up innovation...We have to make a vaccine to stop someone getting infected, 6, 7, 8 years in advance. We are asked to then reconcile our prices, which makes it very challenging."

On Socialism: "I don't think people understand what socialism is. Socialism is when the government controls companies. There is no example where the government controls companies that they do it well and they don't start to use it for votes. They don't want competition. If you have two government-owned companies, why have competition. They do it for jobs and votes. They have bad allocation of capital. They become corrupt over time. It doesn't mean capitalism is perfect."

James Gorman. CEO and Chairman, Morgan Stanley on Economy. "I am always surprised why people are surprised the market is at an all-time high. In a global economy that is growing, by definition corporate earnings are growing. Unless you cut, the market should finish every day at an all-time high. Now of course it doesn't. But if you stand back from a chart, it looks like a straight line, from bottom left to top right." On Banking Sector. "Banks have been the unloved sector over the last couple of years...Historically, I always thought you sold banks at 2.5 times book and you bought them at 1.25. Post crisis at the new capital levels those ratios dropped. We were trading at 1 times book, .9 book. And we just came off record earnings- how is this possible? So the banks have been undervalued and you will see a lot of movement in the bank stocks." On Analyst Expectations. "The questions of 'Did you reach your goals yet? Did you reach them?’ ‘Yeah, we kind of did. So, relax a little bit.’"

Stephen Pagliuca. Co-Chairman, Bain Capital on Private Equity. "There’s a misnomer out there with all the politics: private equity is not about cost cutting, it’s about growth. No one wants to buy a company that is shrinking. And so, we spend all of our time thinking, how do we grow companies? How do we do more R&D? How do we invest in new products?"

Glenn Hutchins. Chairman, North Islands on False Optimism. "The Trump tax cuts were touted to generate 3-4%, the number is now about 2.5%. My main concern back then was that I didn't think adding $1T in debt to our U.S. economy at a time period in which we were in recovery, and should have been reducing the debt load for our future generations, was correct. Countries lose their sovereign credit rating when they take on an immense amount of debt at this period in the cycle. I still have a great deal of concern on the fiscal policies of the administration."

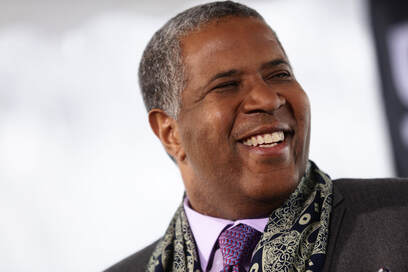

Robert Smith. CEO, Vista Equity Partners on Capitalism. "For the first time since 1930, we have the biggest disparity in both wealth and income, and we have to do something about that." "Capitalism is the most efficient system on the planet for uplifting humanity generally. But of course, in general we go up but we have pockets that do not participate. African-American's have not traditionally participated. In fact you look at the Southern Homestead Act, red-lining around your communities, the inability to actually gain a foothold in the capital part of capitalism so they have always been part of the labor part. We need to drive them through policy, individuals and philanthropy."

Dan Schulman. CEO, PayPal on Cybersecurity. "Security has to be one of the biggest concerns that any business has. The average American business gets attacked 4 million times a year. The average consumer around the world loses an identity or as identity theft every two seconds. So, this is a major problem. Financial firms get attacked millions of times practically every day."

General Antonio Gutteres. U.N. Secretary on Global Tensions. "We live in a difficult period where geopolitical tensions are also having an impact on the economy. Because they generated, as you know, the trade tensions, technology tensions are even bigger in my opinion than trade tensions. And I think that these have slowed down growth and has contributed to the difficulties that the global economy is facing."  Marc Benioff. CEO, Sales Force on New Capitalism. "We are introducing a new capitalism here. Stakeholder capitalism. Which is a more sustainable capitalism, a more equitable capitalism, a more fair, and more just, capitalism. And it’s not like the old capitalism." On Doing Both (Changing the World & Making Money): Everybody realizes that, you know, we’re in a planetary emergency. And we need to make changes. And business is the greatest platform for change. And if you ask what the narrative has been here at Davos, there has been a tremendous narrative around what can we do to improve the state of the world? Making money is easy, but doing the right thing is not. And eventually every company comes to that point. And we’ve seen that over and over again. We don’t have to look at history to understand that leadership eventually is about what you do and who you are. If business is really the platform for change, and you have this amazing tech company platform, what are you doing with it? Are you using it to make the world better? Or are you just using it to make money? And I think that that really is, you know, the choice here in Davos and in some ways, it’s a false choice. You can do both."  If you have made it this far, good for you & I very much appreciate you taking the time! It would be silly to not draw attention to the lack of diversity. A few women, one African-American. The people above, albeit originating from different nations of origin, they all kind of look the same: white males. This has long been the case in executive leadership. These men are all brilliant and have absolutely earned the right to be in their respective positions, I want to make that clear as daybreak. But diversity is important. I think the best, smartest, savviest person should get the job, hands down. But, the world is changing, and we have to change with it. When selecting board members, some companies look strictly for former CEO's. The view above of leadership clearly shows that would narrow the pool in terms of diversity significantly. If certain demographics of people aren't even in the room, how will they have the chance to change the world? I will leave you with what I found to be a very uplifting discussion with David Solomon. For those of you who don't know, he is definitely not your average CEO. He takes the Subway, gets his own coffee and has a side hustle as a DJ. That's not the status-quo. And I think that's pretty cool!  David Solomon. Chairman & CEO, Goldman Sachs on Stakeholders. "You know, our first-priority is to serve our shareholders, to drive long-term returns for our shareholders. But I’m a big believer that unless you take care of your stakeholders more broadly in the medium and long-term, you won’t deliver outstanding returns. So, I think it’s very, very important. We think a lot about, you know, our platforms and things we do, and we try to contribute in ways that we think improve market structure and the capital markets broadly...I think from a governance perspective, diversity on boards is a very, very important issue. And we have been very, very focused on it. And so, we’re trying to find ways to encourage that. And I come from a position of my own experience where I look at the Goldman Sachs board. We have four women out of 11. We have a black lead director. I really value the diverse perspectives, you know, I’m getting which are helping me run the company. I look back at IPOs over the last four years and the performance of IPOs where there’s been a woman on the board in the U.S. is significantly better than the performance of IPOs where there hasn’t been a woman on the board. So, starting on July 1st in the U.S. and Europe, we’re not going to take a company public unless there’s one diverse board candidate with a focus on women and we’re going to move toward 2021 requesting two. And we realize that this is a small step but it’s a step in a direction of saying, you know what, we think this is right, we think it’s the right advice. And we’re in a position also because of our network to help our clients if they need help placing women on boards. And so, this is an example of our saying how can we do something that we think, you know, is right and helps move the market forward?"

2 Comments

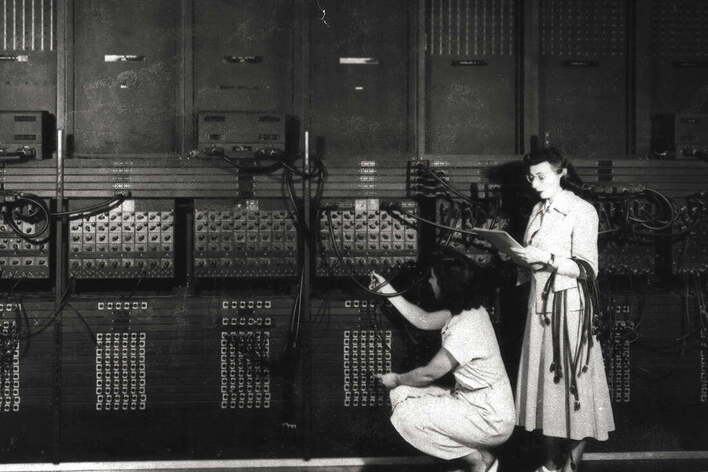

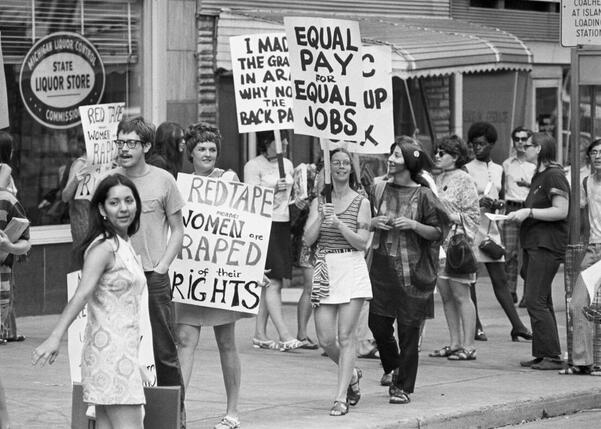

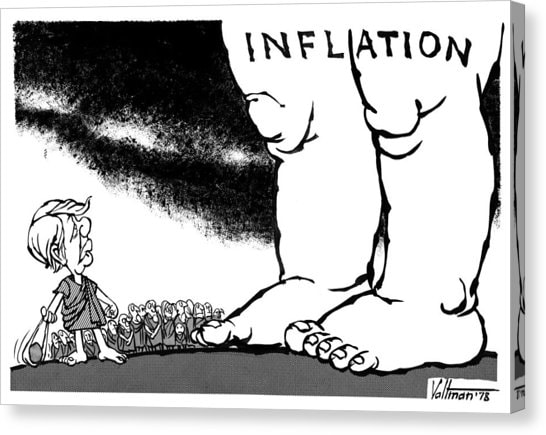

Today, we live in the age of the constant news cycle. 24/7, incredibly fast- similar stories, different day. The Wall Street Journal debuted 130 years ago in 1889. Back in the day, there were no smart phones, televisions or computers to garner the daily stories. Citizens relied on good ole black and white (along with the radio which came about in a similar era.) The old adage goes "history has a tendency to repeat itself." While that may not always be the case, it sure does usually rhyme. It is incredibly important to have a familiarity with milestone events that have led our world to where we are today. The WSJ profiled their most prolific headlines over the past 130 years. I have aggregated them here! Let's go back in time for a bit...  1911. Standard Oil Company is ordered to be dissolved by the Supreme Court citing monopoly status. 1913. The Federal Reserve Board is created. Consisting of 9 members; 3 chosen by the President and the Senate, 3 by the Federal Reserve Banks and 3 by the Secretary of Treasury, Agriculture and Comptroller. The board will be divided into 12 districts, each having its own bank. 1914. The Panama Canal is opened. Steamship Ancon, owned by the U.S., was the first to pass. 1914. On August 5th, Germany declares war on France and Belgium. 1924. Formerly known as "Computing-Tabulating," International Business Machines (IBM) is renamed. 1930. The Smoot-Hawley Tariff Bill passes in the Senate with a 44-42 vote. Raising import duties to protect American businesses and farmers, this added considerable strain to the international economic climate of the Great Depression 1933. Secretary of the Treasury, William Woodin, announces the official abandonment of the "Gold Standard."  1934. President Roosevelt signs into order the creation of the Stock Market Regulatory Board. 1935. The first technicolor movie is presented. 1935. The system of Social Security is established by President Roosevelt (signing seen below.)  1941. The Japanese bombing of Pearl Harbor, Hawaii pushes the U.S. to war. 1944. Initial work on developing the International Monetary Fund (IMF) begins. 1945. Victory in Europe Day, AKA VE-Day, takes place as the Nazis surrender. In the U.S., a scale back of military equipment manufacturing is implemented.  1948. Music is now able to be played via records for an enhanced period of time: 1 1/2 hours, front and back. 1949. AT&T installs over 65,000 miles of cable since the war. Post WWII, over 10 million were awaiting telephone access. 1949. "The Electric Brain" is created. Following the Eniac, which was essentially the first computer, the "Binac" costs around $250K and can compute 12,000 times faster than the human brain.  1956. General Motors profit tops $1B for the first time. 1958. Japanese autos enter U.S. markets: Nissan and Toyota. 1958. The rise of Mutual Funds spur more Americans to invest in the U.S. stock market.  1959. Bank credit cards and buying on credit garner popularity. 1960. The rise of the licensee/franchisee business blooms in the U.S. creating a large increase in income. 1962. Segregation still runs strong as housing developments remain split by race. 1964. The Beatles make their mark on America.  1964. 12-digit phone numbers are developed linking much of the world. 1970. The beginning of women working to end sex bias in the workplace. 1972. Automated Teller Machines (ATMs) are implemented by banks.  1972. The Dow Jones Industrial Average hits 1,000 (it is over 27,000 today.) 1973. The business of "paid TV" rises. 1973. The Cold War reduces the amount of oil flowing to the U.S. from Arab countries. 1975. Social Security is reported to be on track to bankruptcy. 1976. A spotlight is placed on sexual harassment in the workplace.  1977. Computers are no longer only an at-work luxury. In-home computers are hitting the markets. 1977. The origins of balancing a portfolio of stocks to track indices such as the S&P 500 take place known as "Index Investing." 1978. Scientists warn of Antarctic temperatures rising caused by the burning of oil and gas. 1979. Inflation hits record highs as President Carter is set to be sworn-in.  1981. The basis of "supply-side economics" falters as the deficit and interest rates soar as a result of tax cuts. 1981. After it's creation 5 years prior, Apple hits sales of $330MM. 1983. Regional phone companies continue break-ups. One of the 7 entities, Bellsouth, spins off from AT&T. 1986. The topic of the "Glass Ceiling" is raised as top executives are questioned as to why many do not have any women in key, policyholder positions.  1986. The case of Ivan Boesky raises the profile for insider-trading cases on Wall Street. 1987. October 19th marks Black Monday as the Dow drops 508 points in a single-day of trading. 1993. The House approves the formation of the North Atlantic Free Trade Agreement (NAFTA) under President Clinton.  1995. Studies show many Baby Boomers save little and they may run into financial trouble later on (sound familiar, Millennials?!) 1995. Netscape, the Internet server and World Wide Web browser, IPO's. 1996. After leaving Wall Street 2 years prior, Jeff Bezos nabs more than $5M in sales from his online retail business he formed the prior summer. Known as Amazon.com, the main product they sell: books.  1999. A compromise to dissolve the Glass-Steagall Act is reached. This would eliminate financial services restrictions dating back to the 1930's which prevented banking, insurance and securities firms from entering each others respective industries. 2001. In September, an attack killing 3,000 Americans takes place in New York City, Washington D.C. and Pennsylvania.  2002. As Fannie Mae and Freddie Mac have been growing their debt at an annual clip of 25%, they now have $2.6T in debt outstanding. 2005. Colleges fear students are exposing too much personal information on a new site called "Facebook." 2007. Apple announces the intention to release a media-playing, cellphone called the "iPhone."  2008. Crisis on Wall Street ensues as Lehman Brother teeters, Merril Lynch is sold to Bank of America and AIG looks to raise cash- an $85 billion loan later was provided by the Federal Reserve. 2010. Obamacare is voted on and ultimately taken-up. 2015. Investors have poured more than $400M into start-up, Theranos. Promising to run numerous tests from a single drop of blood, the tests able to be performed are much fewer than promised.  2016. In a historic election which has left markets reeling, the U.K. has voted to leave the E.U. 2016. Donald Trump is elected president of the United States riding a populist wave. 2017. The exhaustion of American liberalism as white guilt gave us mock politics based on moral authority. 2018. The China problem is now predatory use of government power to punish foreign competitors to benefit Chinese companies.  What headline will come next? Suppose we will just have to wait and see!

Full link: https://www.wsj.com/articles/130-years-of-history-as-seen-in-the-pages-of-the-wall-street-journal-11562544331 Betches said it best! Here's our best shot at the skinny on retirement savings accounts. Not only will BB&B break down 401(k)'s- but we'll also look at the other options for saving for your future. Prepare to be well informed and never ask the below question AGAIN!  When you're in your 20's, 30's even 40's, retirement may seem like a long ways off. Why should I be keeping my hard-earned money from myself when I could be using it to jet to Baha Mar with my girlfriends (Real Housewives of Beverly Hills style, you know.) BECAUSE, life is hella expensive. You may think life is costly now, but just wait until you're your grandparents age. Healthcare, travel, simply daily life...imagine living the way you do now without an income...pretty tough, right? Hopefully when you're in your 60's, you will be winding down your career (maybe sooner or later, depends!) but one day you (probably) will be in fact living without a steady income (possibly still investments etc. but not a paycheck.)  So, let's put Baha Mar on the back burner for now and talk about saving instead of spending! Will make this as simple & painless as possible- bible. Thanks to the TheBalance.com for guidance on this post.  401(k). A workplace retirement account that is offered as an employee benefit. Basically, thanks for working here, we're going to administer a retirement account for you as an extension of our gratitude. The account allows you to contribute a portion of your PRE-tax paycheck to tax-DEFERRED investments. Good lord, what?! If your GROSS salary (Gross = BEFORE taxes) was $75,000 and you contribute $5,000 to your 401(k)- come tax time, you will only be taxed on $70,000. You can begin withdrawing at age 59 1/2...any earlier, you will be fined a penalty. The maximum annual contribution is $19,000 as of 2019. If you're over 50, you can contribute $25,000. What is the big draw to this? COMPANY. MATCHING. English!? Some companies will "match" up to a certain percent or dollar amount. If your company offers to match up to $5,000- you would be smart to put in at LEAST $5,000. It is essentially free money.  Individual Retirement Account (IRA). This route is chosen by individuals who 1) do not have a company 401(k) plan or 2) you have maxed out your 401(k) for the year and would like to tuck a bit more away. An IRA is used to invest money for retirement in stocks, bonds, mutual funds, exchange traded funds (ETFs), etc. A cool part of an IRA is it truly acts as an investment account- you can buy and sell investments as you normally would. However, the retirement aspect comes into play as you cannot REMOVE money from said account until age 59 1/2, similar to the 401(k). Many taxpayers can deduct their IRA contributions on income tax returns IF they don't also have a 401(k) at work which will reduce their taxable income *there are restrictions* It takes about 15 minutes to open an IRA. You can do so with investment firms such as E*TRADE, Fidelity or the one I personally use, Vanguard.  There are 2 types of IRA's. Traditional IRA. This will be an account invested with PRE-tax money. As discussed above, Uncle Sam will come to collect taxes when you withdraw this money later. Roth IRA. This will be an account invested with POST-tax money. Meaning, your gross sum you are paid will be taxed, then the money will be invested and never taxed again. A Roth is unique as the age 59 1/2 does not apply- you may withdraw contributions at any time without a penalty (with a traditional it's usually 10%.) Note, it has to be at least 5 years after you started the account* Contribution limits to IRA's are low though: $6,000 for both types in 2019, $7,000 if you're over 50.  Roth 401(k). A little combo here! This is essentially a mix of the features of a 401(k) and a Roth IRA. This is similar to a 401(k) as it is offered through employers. This is a new instrument as it gives the Roth aspect of contributions coming AFTER taxes. Same as the Roth IRA, contributions are never taxed again as long as you remain in the plan for at least 5 years. A contingency here, if you're making relatively big bucks*, you may be restricted to contributing. *$122,000 for single filers in 2019 up to $137,000. $193,000 to $203,000 for those filing jointly.  Simple IRA. The Savings Incentive Match for Employees (SIMPLE) IRA is a retirement option for small businesses with less than 100 employees. 401(k) plans are a large reason many people join large firms, therefore, this is a chance for smaller firms to also give a similar draw like the big dawgs. Very similar to a 401(k), the account is made with PRE-tax dollars. Again, the money will grow tax deferred until retirement (it will be taxed upon withdrawal.) The penalty for early removal is the kicker here, if you take money out within 2 years of opening and/or before age 59 1/2, you will pay a penalty of 25%- yikes! One more- you cannot borrow money from a SIMPLE as you can from a 401(k).  SEP IRA. A Self Employed Pension IRA allows you to contribute a portion of your income to your own retirement account if you're self-employed and have NO employees. You can fully deduct these contributions from your taxable income. The maximum contribution limits are higher than the others- for 2019, $56,000 or 25% of your income, whichever is less.  FAQ. Can I have more than one plan? YES. As seen above, you can have a combination. The amount you may deduct from your taxable income will be capped at a certain point though.

Decide how much you're wanting to save and go from there. What if I need to use the money in my 401(k) for an emergency? Most plans offer what is known as 401(k) loans if you find yourself in a bind...this should be a last resort! What if I quit my job? What happens to my 401(k)? At this point, you will have a decision to make:

Should I be saving money besides of 401(k)? How can I put this gently- DUH. The more money you save, the better! If you want to buy a car, a house, a yacht, a plane, a giraffe (you do you)- you need to be saving and investing separate from retirement funds. This money is not to be touched until you're up there in age- so do not rely upon it. It will be there to help you one day but this is not your emergency fund. Think of it as your nest egg but also don't think of it at all. Just ensure you're contributing and not leaving money on the table.  Off to Davos global executives, world leaders and members of the media went this week! This was one of my favorite posts last year so figured I would do it again as the Global Risks Report by my employer, Marsh & McLennan Companies, has just released the 14th edition for 2019. The World Economic Forum (WEF) is a Swiss non-profit foundation. The international body cites it's mission as "committed to improving the state of the world by engaging business, political, academic, and other leaders of society to shape global, regional, and industry agendas". In layman's terms, it is a gathering of about 3,000 businesspeople, celebrities and journalists to discuss the state of the world. The theme for the 2019 forum is "Globalization 4.0: Shaping a Global Architecture in the Age of the Fourth Industrial Revolution." Marsh & McLennan Companies are instrumental in helping put together the Global Risks Report. The report is about 100 pages discussing the worlds largest risks. I think it is vastly important to be aware of the emergence and development of these risks overtime. In this post, I am going to present a synopsis of what was included in this years report.

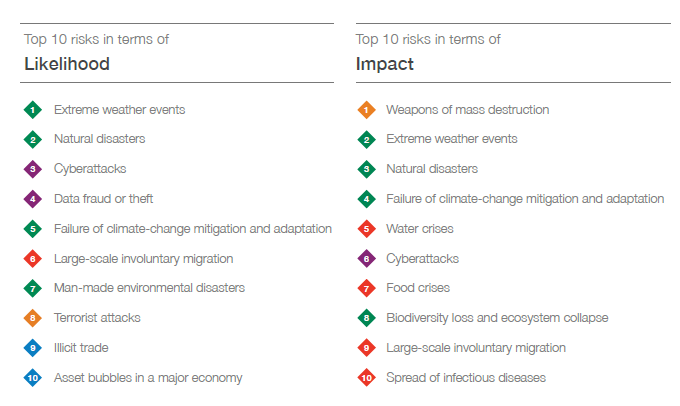

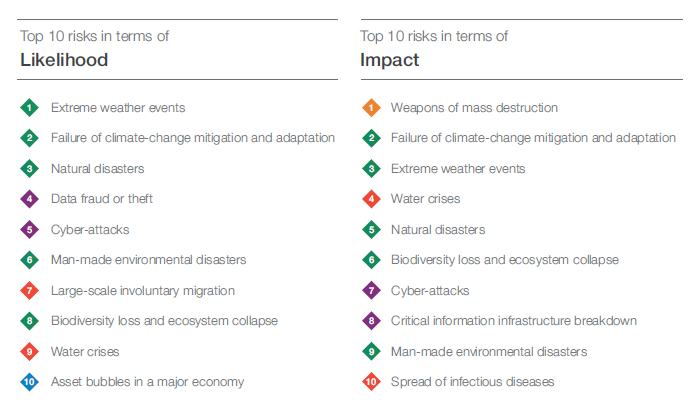

The report begins with the largest risks our world currently faces: individuals, companies, governments, etc. The first, is from 2018. The second, are 2019's most pressing risks. It is always interesting to see how these change form year to year. You will note, cyber and natural disasters are always near the top of the list. We will delve into some of these below.  Macroeconomic. Financial market volatility increased as fears over the future of global economies rattled investors and central banks alike. The latest International Monetary Fund (IMF) prediction shows a gradual slowdown over the next few years. Historically large economies (ex: China) have lowered growth estimates. The global debt burden is also continuing to rise as it began post the 2008 financial crisis. Geopolitical. Rifts between major powers have been increasing- notably the United States and China. A period of globalization has taken place which has altered the political economy globally. A concern arising: should a global crisis take place, would the mega powers of the world be able to join and work together for a collective solution. Environmental. A range of environmental issues are at the forefront: extreme weather, agreement on proposed climate agendas, loss of species that could alter the human food chain. For humans, loss of biodiversity effects health and socioeconomic development as it can spur malnutrition. Disruptions in the delivery of goods or services due to a natural disaster is also a large concern. Technology. Data fraud and cyber attacks continue to be high on individuals and corporations list of concerns. The likelihood and potential severity of these attacks on companies computer systems have increased with further emergence of technology. The enhancements of artificial intelligence, while in many ways better our world, pose a threat to societies if not monitored. Technology is also seen as a major loss of privacy and deepening polarization. Energy Grid. The number one threat to our world, as stated by the U.S. Department of Homeland Security, is an attack on our energy grid by some sort of cyber malware. Utility companies spent an estimated $1.7B in 2017 on protecting their firms from such an attack. Many agree that in the future, there may need to be a government backstop (to cover expenses as TRIA does for certified acts of terrorism that was instated post 9/11) if this were to happen because no individual company (ex: ConEdison) could sustain the damages.  Oceans. Ongoing climate change and rapidly growing cities continue to make humans more vulnerable to rising sea levels. Urbanization, or the move to cities, exacerbates the risk of destroying natural sources of coastline resilience and put an immense strain on groundwater reserves. Rising oceans pose a risk to over consuming roads, railways and ports. Internet cables running deep below the grounds surface also could be damaged due to excess water. Sanitation along with drinking water becomes a concern should ground water be contaminated by salt water. This also contributes to damaged agriculture. Mental Health. Issues ranging from anxiety to depression and beyond effect an estimated 700 million people worldwide. The decline of well-being is, in itself, a risk as it contributes to the degradation of social cohesion and political landscape along with society productivity. Biological Threats. A release of biological pathogens is widely thought of as a prime terrorist attack scenario. However, these also could be accidentally released. The vitality of having cures for said diseases along with prevention and contingency plans are a key risk mitigation tactic. Intentional biological trends including genetically modified babies is a new frontier requiring monitoring. Income Inequality. Widening levels of wealth disparity and divergences between public and private levels of capital ownership are exacerbating the gap between the classes. The transfer of public to private wealth has occurred in nearly all countries whether they be developed or emerging. Underlying effects become a lack of cohesion and seemingly a distrust in the system. Identity Politics. Immigration and migration changes has played a large role in asylum rules and regulations. The rise of the #MeToo movement put the notion of discrimination against gender front and center in industries ranging from Hollywood to Wall Street. Women are also more likely to be displaced from their jobs due to automation.  Globalization. Powers of the world have shifted. World leaders have changed as have the bodies in which they oversee. In relation to states, the following has been taking place: individuals have seen less control as states tend to be the reigning power. Along with companies, many are controlled by the states to the extent in which is the highest percentage seen in decades. Multilateralism. As variables including GDP continue to evolve and change, multilateralism and the powers that be also must do the same. The idea of states forming an alliance to pursue a greater good , in theory works. However, with economies and political powers evolving, these formations need to be revisited. Trade. China and the U.S. are arguably the biggest story in this arena. However, they truly are just a fragment of the larger puzzle. Although large economies such as these may influence global growth, smaller countries also play a role. With tensions escalating, the Internal Monetary Fund has revised growth projections for 2019 by 20 basis points. Tariffs on everything from aluminum to washing machines to European cars- the notion of “economic security being national security” is at the forefront for many countries as they evolve as more protectionist. Investments. Monetary investment in governments, sovereign wealth funds and in particular, strategic sectors, have been blocking investments in emerging technologies. In August of this year, Germany announced a reduction in the threshold at which foreign investments can be blocked. If citizens of one country do not believe in their homeland’s trajectory, they will seek returns elsewhere. The balancing act arises when citizens of that country want to invest and the opportunities have been saturated with outside investors. Foreign Direct Investment. Also known as FDI, the make-up of where this aid comes from for projects including infrastructure has changed from more traditional to outside governments stepping in. The issue comes as FDI is continuously becoming more politically charged.  Anger. While not as tangible as other topics touched upon in the Risks Report, every year Gallup takes a poll of the world's emotional state. As you may guess if you turn on the television from time to time, we are living in a very divided world. This leads to a "tremendous increase in mutual hatred." People reporting themselves as "angry" or more "on edge" on a daily basis rose in the past year. To blame? Shock: politics ranked as one. Families have been divided and at times stopped speaking on account of disagreements. To quote- "incivility has boiled over because we have lost respect for opinions other than our own." Let's take a step back, my friends. Social Media. Specifically SM but really technology as a whole has been working it's way into become a full-blown addiction for many. This is the leading cause for feelings of isolation and loneliness. The blurring line between reality and fiction continues to become more opaque. Related to this is lack of sleep, poor performance in work or school and an immense decrease in in-person interactions. Workplace Stress. A large number of workers globally attribute being overworked with their lack of happiness in their jobs. Other factors include ergonomic stress or lack of a work environment that provides comfort. Many report a constant stress is the creeping up of automation and the fact many jobs will be replaced by AI in the coming years. ^These may not seem as serious as inflation or an impending recession, but people are what make up our world. If we live in an environment where individuals are constantly anxious and angry, the long term effects will indirectly influence most of these other topics in some form or fashion.  Outbreaks. The spread of infectious diseases across the world have been occurring with increasing frequency. Five trends have been driving this: surging trade can pass diseases into different parts of the world by both humans and food contamination. With 55% of the world living in urban areas, high density living enhances the risk of disease spreading. Deforestation has been an issue in countries such as Africa where diseases are spread via mosquitoes and other various animals. Climate change has been linked to a rise in the transmission of diseases including dengue fever. Finally, human displacement. When thinking about the Syrian refugee crisis, humans migrating and generally in rough conditions and close confines once arriving at migration camps have led to outbreaks. Healthcare Costs. While healthcare is advancing and less lives are being lost because of modern medicine, these potions to cure sicknesses come at a hefty cost. Procedure and prescription costs have skyrocketed leading to an increase in the cost of healthcare. Without insurance provided by your employer, it can be very difficult to stay ahead of healthcare expenses. Pathogen Preparedness. Speaking on biologic threats above, the World Health Organization is proactively preparing for worst case scenarios. Should an attack of sorts take place where a pathogen is released, how would the WHO be able to ensure the disease is contained and then not passed along to both doctors and other citizens.  Disaster Recovery. Over the years, we have seen an increase in the cost of disasters. Notably expensive storms, hurricanes Harvey, Irma and Maria, the cost for spending post a disaster is almost nine times higher in many cases than on preventing the disaster in the first place. Why are the storms costing more? Are storms getting worse? Possibly. Frequency ebbs and flows. But a key factor is simple: there is more STUFF! There are more homes than in the 80's. More businesses, cars, bridges- more things that can be wrecked causing an increase in recovery costs. Waste. Population growth clearly exacerbates food availability. To sustain current food levels between 2019 and 2050, this will require a 70% increase in food production. Coupled with other issues mentioned above- this could be a tall order. A large issue has to do with the amount of food wasted- particularly in Western civilizations. 95 kg's of food is wasted per person every year in the United States. Compared to Rwanda? 1 kg. Food Insecurity. You've heard of the trade war between the U.S. and China- mainly steel, aluminum. There is also the potential for a food trade war in the future. Cross border issues can block certain goods, unable to be grown or produced in a country, from entering. If an ecosystem in one country fails, they may be entirely reliant upon a neighbor. A tense conflict could limit accessibility.  Supply and Demand. As we spoke above on the trade war, there are sometimes unintended consequences of tariffs, etc. Imposing tariffs on certain goods may bring another government to the negotiating table but as seen with Chinese goods, these tariffs then make U.S. products more expensive. Why? Supply and demand basics. If you cut off the pipeline of semiconductors for iPhones that come from China (and are generally cheap) you are going to have to find somewhere else to get said components- usually from a more expensive source. Fracking. Similar to the above, you're facing what some environmentalists consider a trade-off. While reports of fracking directly causing earthquakes is largely unsubstantiated, many see our energy independence which was shepherded by the Bush administration as a trade-off to environmental harm. The United States is now a net exporter of energy for the first time in years. Currently with an oversupply of natural gas and a healthy pipeline of crude, studies will need to continue to be done to ensure if fracking is ceased because of these concerns- that it will be worth the price the U.S. will pay to go back to being energy dependent. Space. The amount of government and commercial activity in space has been increasing rapidly. The concern is of course an actual collision but second that it could become a potential battleground.  As you can see, Davos is chock-full of discussions and gives a good feel of sentiment for the year ahead. I will leave you with a few interviews with the CNBC anchors and some of the most influential business people in the world.  Jamie Dimon. Chairman and CEO of JPMorgan Chase.

David Solomon. CEO of Goldman Sachs.

Ginni Rometty. Chairwoman, President & CEO of IBM.

Christine Lagarde. Chairwoman of the International Monetary Funds (IMF).

James Gorman. Chairman and CEO of Morgan Stanley.

Majid Jafar. CEO of Crescent Petroleum. "Oil prices are more likely to hit $90 than $40 in 2019." Mark Weinberger. CEO and Global Chairman of Ernst & Young. "The government shutdown will not have a long-term effect on GDP." Jim Coulter. Founder of TPG. "The economy is like a frat party at 4 AM- late, but not over." Bono. Singer, U2. "Capitalism is a 'wild beast' that if not tamed, can chew up a lot of lives." Jes Staley. CEO of Barclays. "We'll likely be uncertain about Brexit right down to the wire." Ray Dalio. Founder of Bridgewater Associates. "Capital could flee the U.S. if Alexandria Ocasio-Cortex's tax idea becomes a reality." Marc Benioff. CEO of Salesforce. "San Francisco is a train wreck of inequality because of Silicon Valley."  So, this may have seemed like a bunch of gloom and doom but I will leave you with this. James Gorman spoke on his notice during Davos that the more he spoke with other business titans and global leaders, that somehow the conversation turned more negative than our reality really is. He said you can seemingly talk yourself into thinking the world is worse off. Jamie Dimon followed this with, of course, the world isn't perfect. But what are we, WE, as individuals doing on a daily basis to make it better. Take it all with a grain of salt and keep on a'goin', one day at a time. "Look up at the stars, and not down at your feet. Try to make sense of what you see, and wonder about what makes the universe exist. Be curious."- Stephen Hawking Sources:

Marsh & McLennan Companies Zurich Insurance America CNBC Google Images World Economic Forum Group of 20  So, yeah, about that budget... The holidays are right around the corner and many are prepping their wallets for large spending months in the near future. From Market Watch, Americans racked up on average $1,054 in the 2017 holiday season. Half of people could pay off in 3 months. 29% would take more than 5 months. 10% would only be able to make minimum payments on their credit cards. THIS. IS. BANANAS.  Before we get into some tips and tricks to get the most bang for your buck- let's begin with the trite notion of not living beyond your means. Warren Buffett stated this in regards to stocks but rings true in daily life. "It is insane to risk what you have and need in order to obtain what you don't need." If you have lost your job, you don’t need to be spending on family members as if you still have an income. Buying your child the newest pair of Nikes could mean not being able to put food on the table at some point. It may be a tough conversation but as adults, we have to recognize when you may be in a difficult financial situation and it is necessary not to overextend yourself and end up in financial despair.  And, of course, I will follow that advice with a photo of a Gulfstream only because it's way prettier than a Delta Airbus 320. HOLIDAY TRAVEL. Mix and Match Flights. Sites like Priceline can mix and match airline carriers in order to get you the best deal. Possibly one leg will be on United and another on American. Maybe you will have a connection. Every little saving helps when you will be traveling for possibly both Thanksgiving and Christmas (Hanukkah, Kwanzaa- whatever your jam is.) Cab It. If you’re flying, maybe Uber to the airport depending on how long you will be gone and how expensive parking is- those tabs can add up. Skip the Luggage. Try to pack only carry-on’s to save from 1) your luggage being lost at a busy time of year but 2) the bag fees that are going up. Most airlines now charge $30 for your first bag and $50 for the second. Multiply that times two for a round-trip. Road Trip! Close enough? Skip the flight and drive. Oil has been at record lows due to oversupply making gas prices pretty cheap.  HOLIDAY ENTERTAINING. You are the host with the most! It is always gracious to host a holiday. A lot of planning is involved and usually a LOT of money. Food, drinks, decor, the little things can really add up. Have a plan for how much food you will need. Try and buy in bulk to save if you're entertaining groups of people. Also, if people are staying at your home, use the leftovers from the night before to make breakfast the next morning. Eggs with hams and leftover veggies is not a bad idea. You can also use that leftover champagne for mimosas ;)  HOLIDAY SHOPPING. Set a Budget. 1st step is to determine how much you can comfortably spend. Look at your upcoming expenses, current credit card statements, bank account and form a plan from there. Make a List. Begin with a list of items you are buying for friends and family. Write down the item and how much you hope to spend *stick to it!* I will spend $x on the kids, $x on my spouse, etc. A Deal Isn't Always a Deal. Cool your jets on the “deals” your getting during things like Black Friday. Keep in mind stores use a technique called “anchoring” to make you think you’re getting a crazy deal. Most retailers mark-up items about half. Meaning if they paid $50 for a product, the sales price will be $100 (minimum- lots of stores mark up even more.) So when you see that glimmering 20% off- know that isn’t REALLY a deal. It’s anchoring. It is telling you the price WAS $100 and now its only $80- when in reality the item is worth $50. Of course its always better to save a bit of money if it’s something you’ve really been hankering. Just don’t get tied up in thinking you have to buy something because you’re getting some crazy, amazing deal. Get Creative! Save your bucks and DIY! Head to a craft store and come up with a unique idea. My friend Catherine used her Polaroid camera to snap pics at parties over the holidays and then got inexpensive, cute frames to put them in and gave those as gifts. It’s the thought!  TIPS & TRICKS. Cash Only. Roll like Migos and Ellen and stick to cash. Hit your bank before the mall and withdraw your chosen an amount, of say $600 to spend on gifts, remove that in cash and don’t touch that card! Using cash makes you more cognizant of what your spending. Migos keep like $100k on them at all times so maybe do a bit less than that. Clip the Coupons. For online, look for free shipping and discount codes. For in store, look to see when their sales are starting. Also, check their websites before heading to the physical store as they might have coupons to be used in store. Prepare for Pop-Ups. Buy a few generic gifts. If someone drops by a present and you feel obligated to give one back- it’s nice to have a couple spare candles or bottles of wine to give in return.  Just remember what the holidays are really all about...ALCOHOL *kidding*- - my family does take it pretty seriously though as you can see above ;)

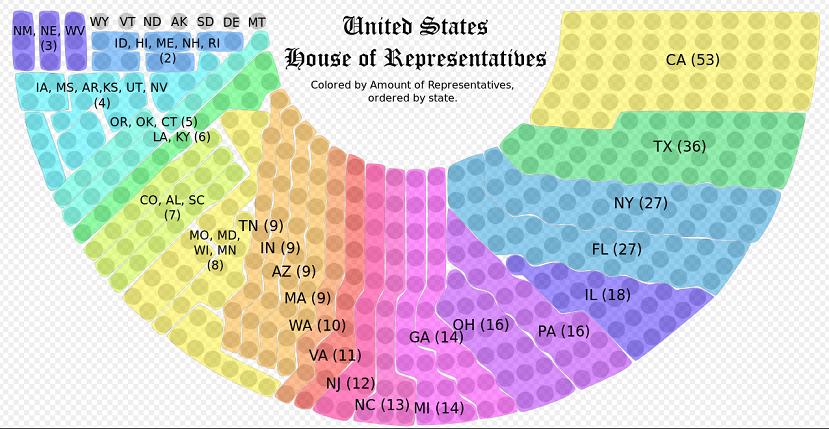

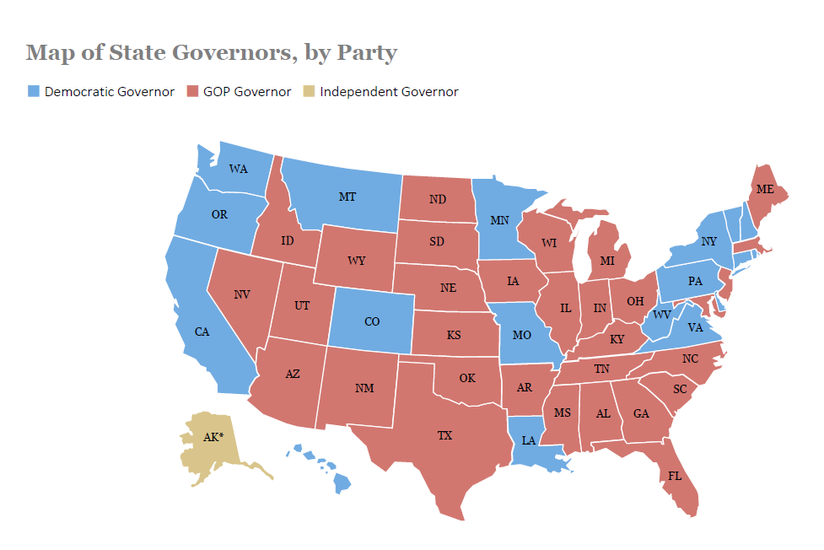

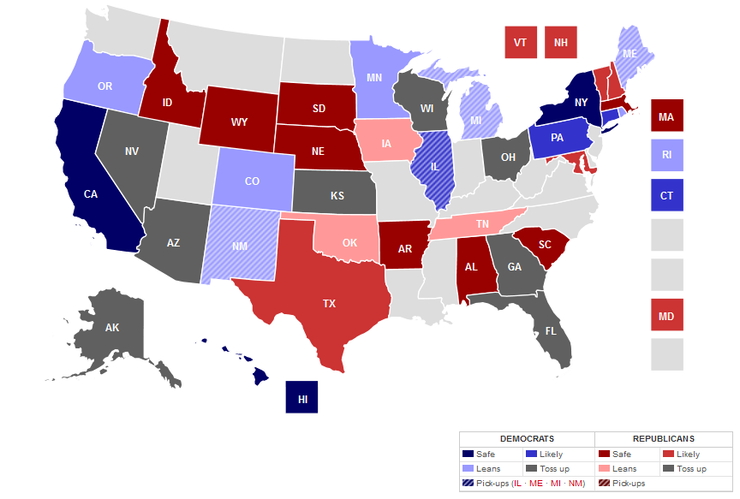

Overall, don’t get so wrapped up in “stuff.” It is hard work to make money. Throwing it away frivolously on things you don’t really need is just wasteful. Maybe if you all have enough “things” find a charity to donate to. If you want to do good without spending any bucks, go volunteer. These holidays tend to be about excess and when you’re done it can be pretty exhausting and depressing if you’re going to return to a bank account with 23 pending charges. Be smart. Your friends and family will love you no matter how big or small the gift is. Sometimes the gift of just all being together is enough. Happy holidays to all of you and your families! xx, SH  2016 was pretty exhausting. Political ads, debates and family fights at the dinner table over who was voting for who. Well, phew, thank God we don't have to do that for another 4 years. Eh, not quite. Although we will not be electing another president in 2018, this coming November, there will be midterm elections for congressional and gubernatorial seats- and it's bound to get interesting with the current climate.  I am writing this piece for Barneys, Bergdorfs & Bill$ readers, but also for myself. There are many upcoming elections- it can be hard to keep track. Hopefully this serves as an all-encompassing, brief breakdown of what is to come. Let's start with the two branches of Congress: the House and the Senate.  House of Representatives. There are 435 seats in the House. The length of these terms is 2 years, therefore every mid-term year and presidential election year, every single seat will be up for grabs. 218 seats are needed in order for one party's control. The number of seats each state is entitled to (seen above) is based on that state's population. Large states such as California, have numerous seats (53). Smaller states including Vermont and Wyoming only have 1. You may have heard of certain elections that have already taken place- these have been in rare instances where House members have resigned or, for any other reason, left their post early. The majority will be elected on November 6, 2018. The representative you vote on is dependent upon the district in which you live. For example I live in the 12th Congressional district of New York based upon my address. Your ballot will already have the district selected.  The Senate. Every state regardless of population has 2 state senators. Some states, the senators are split between political parties whereas others there are 2 Democrats or 2 Republicans. Currently the U.S. Senate is occupied by 51 Republicans and 49 Democrats (including 2 independents) who will occupy the position for 6 years. In 2018, 35 seats are up for election- 26 are held by Democrats. The Democrats will need to gain 2 seats to take control. On a local level, states will have local Senates and Senators. These individuals are largely there to work on local issues for their districts.  Gubernatorial. AKA the race for Governor. Each state has one governor. The current breakdown is 33 Republicans, 16 Democrats and 1 Independent (Alaska). Terms are 4 years in each of the 50 states besides Vermont and New Hampshire where terms are 2 years. The map above was the breakdown of governors by political party in 2016. There will be 36 gubernatorial elections in 2018, as seen in the highlighted map below. As you can see, Nevada, Arizona, Kansas, Wisconsin, Georgia, Ohio and Florida were all Republican in 2016 and now are considered toss-up's.  Other than the elections mentioned above, there will be races for attorney general, state comptroller, etc. Campaign sites are a great way to get a solid understanding of the issues at hand and candidate stances. So what's going on right now? As per a recent article in the WSJ- Democrats are banking on strong turnout this fall to reverse President Obama-era losses that left Republican governors in a near record 33 states. Republicans are defending 26 of those governorship's this fall. The Republican Governors Association has raised $113M and Democrats with $67M. The gubernatorial elections are particularly important because of years past in Washington, lots of policy making decisions have been pushed to the state level. A large importance is a candidate for governor being endorsed by the President. In the primaries so far- President Trump's favored candidates won the nomination in Georgia, Michigan, Kansas and Florida.  In the House, Republicans are trying to prevent a blue wave. A big question for the states is how popular is President Trump in their district? The more popular- the more likely the seat will remain or flip to red. History has a tendency to repeat itself- last time a president's approval was as low as President Trump's, President George W. Bush's administration lost 30 seats. Democrats may have the wind at their back but they still need to flip 23 seats to take the House majority- and that is no simple feat. In the Senate, the terrain is vastly different than the House as it is a very red battleground. 10 of the Senate Democrats up for re-election in 2018 represent states that President Trump won in 2018.  You can still register to vote (*note originally published in September). In most states, papers and voter information must be done 15-30 days before an election so don't wait too long. Summer is already over and November will be here before we know it. Check out the Voter Registration website to learn more and check when your states requires you to be registered here.

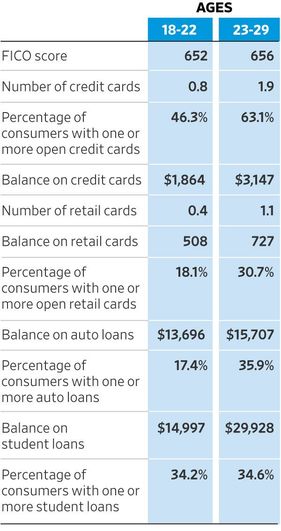

Also, Refinery29 put together a guide of what you need to vote and other election day information. Finally, there's a lot of "fake news" out there. A good go-to guide is 270ToWin where I got a lot of the information in this post. Hope this provided a brief breakdown of what to expect in the coming weeks. Always remember how lucky we are to live in a Democracy where our voices are able to be heard. Not everyone in the world has this privilege. xx  School is back in session! Now, guaranteed, college kiddos are far more concerned with Animal House like ragers at KA than which credit cards are going to help them down the road. But let's put these Natty Light and chicken-on-a-stick purchases to good use, shall we?! There was a great piece in the WSJ today titled Year-by-Year College Education in Credit Scores.  How can students use their four years at school to build a good credit rating and put themselves in a better position post graduation. Let's start with the stats above. A 22-year-old has a FICO credit score of 651 (the range is 300-850) on average and $2,012 in credit card debt. Generally as students get older and graduate, they open more credit cards and then rack up more debt as their lifestyles become more expensive and "adulting" begins.  So, let's break this down year-by-year with some tips on how to multi-task your partying, I mean studying, with building for your future. Freshman Year. Baby steps- parents can add their child as an authorized user on one of their credit cards. Warning to only do this if the parent themselves has a good credit score. If the parent doesn't, this could end up hurting your student from the start. Also, maybe have the talk of what justifies an "emergency" or else you could get some mass bar-tabs from Thirty Thursday. Oh wait, the drinking age is 21- never-mind! ;) The 2nd option which distances parent from child is a secured credit card. This card works essentially as a debit card as it is funded by depositing cash. The student would spend his/her money each month and then replenish it after paying the bill. 18 is the age at which students are able to begin requesting their credit score information. Using Experian or a similar credit bureau can help them understand how credit is built and why it is important.  Sophomore Year. Headed back for year 2! At this point- some kiddos might have a car by now- maybe not a Porsche like Elle Woods but making car payments on anything getting them across campus to that astronomy lab. Parents may be making the car payments while students pony up for gas- better for their credit score- flip this arrangement! If the student cosigns and makes said payments, it will help them down the road. However, most kids are focused on school and maybe don't have a part-time job so this burden could be too heavy. Evaluate your families personal situation and go from there! Paying cell phone or utility bills formerly haven't helped credit scores. However, students living off campus can now use Rental Kharma or ClearNow to have those payments reported to bureaus (albeit, make sure they are being paid in full and on time.) First unsecured credit card- try and gas or retail credit card the author says! Keep the balance low- never more than 30% of your credit line even if you're able to pay off more.  Junior Year. Classes getting a bit harder now, eh?! At this point- if students can make a small dent in that student debt, they will be money ahead. Even if more loans are going to be needed, any payments will be reported and can help credit scores. Keep trying to move forward with your credit cards as well. If you haven't graduated from your parents CC, try a secured CC, if you have a secured CC, try a retail or gas card. Retail or gas card? Try a full credit card from your bank.  Senior Year. Almost there! If you don't have a credit card at this point- definitely apply based upon your personal situation. Underwriting standards make it easier to get a card albeit the limit may be lower. If you have a card, try and negotiate for lower annual fees or APR. Although having a lower APR will save you money, the best way to save money is simple: be able to pay your bills every moth. It's not always possible for everyone and we recognize that. But life will be much easier if you don't start off with student loans AND credit card debt. Loans may be inevitable but daily spending is up to you.  The road after this is an exciting one. There will be peaks and valley's and sometimes being an adult is going to hit you hard but everyone has to grow up! There are ways to make your life easier or harder and keeping a level-head on your spending will surely ease your anxiety for the years to come.

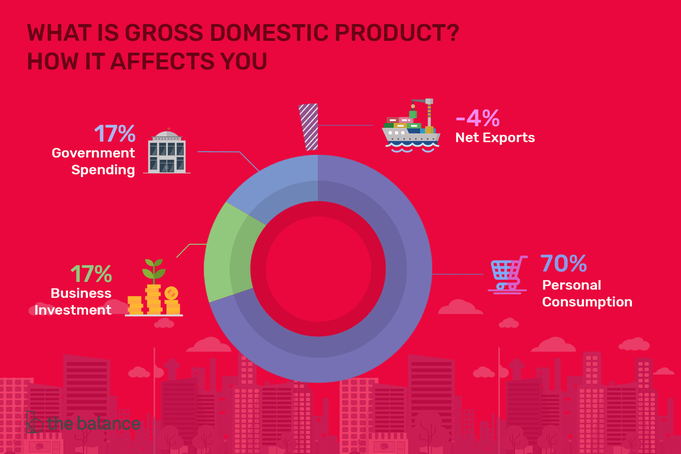

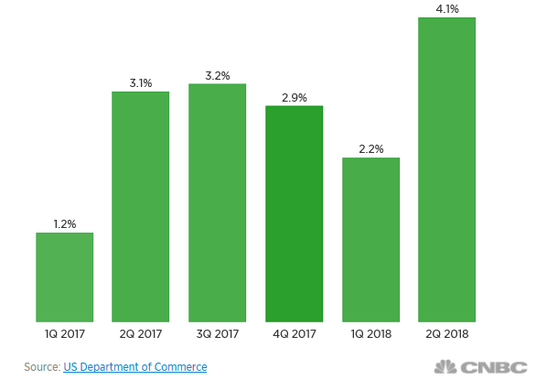

Living in debt because of irresponsible spending or simply just not making cognizant efforts to stay in good financial standing will hurt your ability to provide for your family in the future. Everyone has a different situation and some are much more difficult than others. But really, don't make your life harder than it needs to be. Make a concerted effort to control your spending, borrow wisely all while enhancing your credit score will lead to a much nicer life. xx  Fan of the president- not a fan of the president. Doesn't matter. But there are certain things we Americans cannot deny. Like the fact our economy is thriving. Whether or not you think President Trump is responsible for this is beside the point. I think it is vital to understand what is going on fiscally in our country as social issues tend to take over the headlines and the state of our country can seem a bit, well, depressing. Fiscal stories are what some, well, maybe lots would deem boring. Here is brief (hopefully not confusing) synopsis of how the American economy is doing:  Today, Gross Domestic Product (GDP) numbers were released for the 2nd quarter of 2018. GDP is released for each of the 4 quarters of the year (similar to companies- although corporations fiscal years may not begin in January.) 1st quarter = January 1st -March 30th. 2nd quarter = April 1st - June 30th...you get the idea. GDP is detailed in Barneys, Bergdorfs & Bill$, but basically it is the best way to measure a country's economy. It is the total value of everything produced by all the people and companies in the country- if they are located within a country's boundaries, the government counts that production into GDP. Gross Domestic Product = Personal Consumption Expenditures (how much Americans spend on goods) + Business Investment + Government Spending + (Exports - Imports)- - hang in there, this gets simpler.  Nominal vs. Real GDP: real values are adjusted for inflation, nominal values are not- with this, nominal GDP values will appears higher. Inflation: the rate at which the general level of prices for goods and services are rising. When inflation rises, the power of your currency (our dollar)- falls. Don't let the words confuse you- it may seem complicated but the principle is simple. Understand inflation is why people invest their money. They invest to make a return. While it may seem more safe to stash your cash in your bank account- due to inflation, your money is devaluing. The goal is "price stability." Not too much inflation, not too little.  So what did today's report say and what does that say about our economy? First half of 2018 results:

What else?

Tariffs. You have no doubt heard the conversation revolving around tariffs, most notably, the battle with China. So what's the skinny and how does this factor into our economy?

In a nutshell:

And as you can see above, not everything is hunky dory but overall, fiscally, things are going well.  It is easy to be consumed by the "gloom and doom" on newspaper headlines and mainstream news. These stories sell, and don't get me wrong, obviously not everything in this country is going swimmingly, but these figures released today are something Americans should be proud of. You can credit whomever you like with these successes. I tend to agree with the idea that if things are going well, Presidents may get too much praise. If things are going poorly, Presidents may obtain too much flack. A lot of what goes on is not necessarily a direct result of their actions but a combination of many elements and potentially have been years in the making.  The soon to be retiring CEO of Goldman Sachs, Lloyd Blankfein, said this at the World Economic Forum in Davos, Switzerland this past January and I think he nailed it: I like a lot more stuff than I don't. The stuff I don't like is not as substantive. Some of it is, and some of it is social aspects. I've said this, but I don't want to be hypocritical either. I've really liked what he (President Trump) has done for the economy and I think he's gone out of his way to be very, very supportive of the system. Frankly, I want to honor that. We are America. CNBC

Investopedia The Balance Google Images  I'm not a huge TV person. I'll engage in a couple guilty pleasures- Real Housewives, I'm shamelessly a sucker. But I tend to stick with financial news on CNBC. As far as shows go, I migrate towards anything having to do with business. Succession on HBO is a newbie but, in my mind, there is absolutely nothing that touches my absolute obsession. Billions on Showtime.  The main character, Bobby Axelrod is the hedge fund magnate behind Axe Capital. It is hard not to desire and be in awe of this Metallica blasting, sports car driving, multi billionaire alpha male. A crash-pad with sweeping views of Manhattan to his Greenwich home base to a palatial pad in Southampton on Meadow Lane, he makes what he coins "F you money." Many draw parallels to former SAC Capital boss, Steve Cohen. SAC Capital was fairly synonymous with insider trading. In 2010, the SEC opened a case. By 2013, the firm had plead guilty to the charges and many indicted. If you are familiar with the case and enjoy the show check out, Black Edge.  So is he corrupt? Yes. This is the entire premise of the show. How close to the law can you skirt before you get caught. How manipulative can you be to make an immense amount of money while keeping the SEC off your scent. As narcissistic as he seems, he is a fairly likeable character many would say. He is the face of capitalism. Coming from nothing, he worked until he made it. Caddying for arrogant businessmen who now ask him for money. The show has celebrity cameos from real life business tycoons- the likes of Sara Blakley of Spanx to hotelier Jonathan Tisch to Avenue Cap boss Marc Lasry. The show is complicated with life, business and the insatiable desire to live on the edge. Incredibly accurate & well written, the Showtime original is directed by a slew of people familiar with financial markets, of which include Andrew Ross Sorkin of CNBC's Squawk Box.  This show is riddled with pithy one-liners that serve as major business motivation (the legal way, let me clarify.) Here are a couple quotes that embody the power, drive and lust for more that have shaped the first 3 seasons. "You don't have to outswim the shark. You just have to outswim the guy you're scuba diving with." "No one quits while they're ahead. This isn't France. It's America." "Calculation is not something to be scoffed at. It's a tool. A tactic. And I use it proudly and often." "I like nightmares. When I wake up, they leave me deeply valuing my reality." "You know your shopper isn't your friend. Your personal trainer doesn't actually think you're making progress and all the charities you give money to don't actually honor you when they honor you." "The fact you can't fully understand that doesn't mean he's wrong. It just means you haven't gone beyond your own limits." "Foolishness is right next door to strength." "A lot of guys watch Bruce Lee movies. Doesn't mean they can do karate."  "You don't try to be loyal. You just are. Or you're not." "Get good at letting go, which is a different kind of freedom." "It's not easy to do. But people are at their best when they feel appreciated." "Meaning matters more to me than happiness." "When did it become a crime to succeed in this country? People used to want to be the guy in the limousine. They still do. But now they throw eggs at it." "The greats never sacrifice the important for the urgent. They handle the immediate problem and still make sure to secure the future." "Nobody leaves a negotiation happy." "What is it you do that you're the best in the world at?"  And the grand finale:

"What's the point of having f*** you money, if you never say f*** you?" "The moral of the story is, you get one life, so do it all."  The old adage of two brains being better than one still rings true. I mean, look at these two fellas. Bill Gates has long championed Warren Buffet as being his mentor. Not a bad choice. Some have one mentor. Some have two, ten... No matter the number, one way to think of these mentors or people of admiration is your "personal board of directors" (P.B.O.D.) Every company, public or private, must have a least one director. The mandate of said director, or directors as per Investopedia, is to establish policies for corporate management and oversight, making decisions on major company issues. Within public companies, the B.O.D. represents the shareholders. But that's for the company. What about for you?  In this weekend's Wall Street Journal, Microsoft Executive Vice President of Business Development, Peggy Johnson, lent her insight into the people she leans on as her system of checks and balances. "She largely relies on her gut when making big decisions but then 'validates her intuition' by checking in with valued former colleagues, mentors and family as independent advisors." From a former colleague at Qualcomm, to the CEO of Ulta Beauty to the President of Liberty Media who helped her adjust when she was appointed to her first board seat, Peggy has stacked her roster full of people who have supported her & whose opinions she deeply values. You only know where you've been, therefore it is vital to tap into and develop genuine relationships with those that may not always know MORE than you, but have had different experiences than you, or have been around the block a few more times. Check out some famous duos below and their testaments to the value of a P.B.O.D.'s.  Sir Richard Branson. Founder, the Virgin Group. Mentor: Sir Freddie Laker. Founder, Laker Airways.

Oprah Winfrey. Chairwoman and CEO, HARPO and the Oprah Winfrey Network. Mentor: Maya Angelou. American poet, Civil Rights activist.

Tim Cook. CEO of Apple. Mentor: Steve Jobs. Former CEO and Founder of Apple.

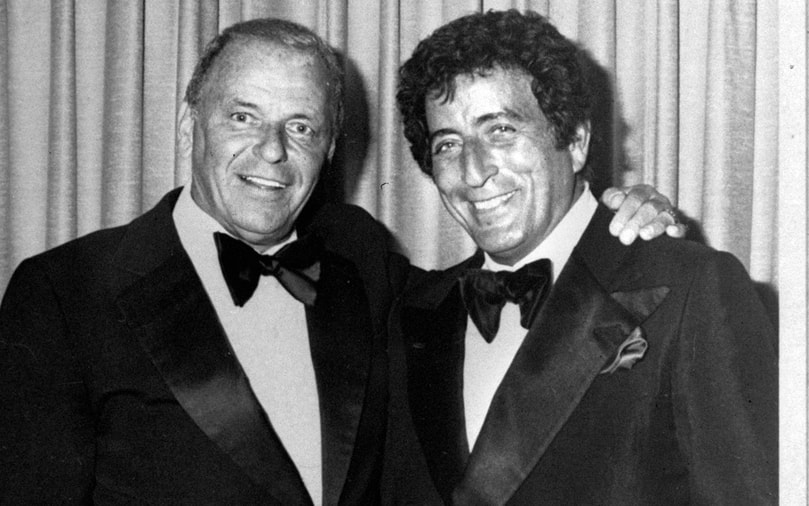

Tony Bennett. Jazz musician. Mentor: Frank Sinatra. Jazz musician.

The lessons learned from mentors are endless. Configuring a personal board of directors will pay major dividends down the road. Who knows, you might even succeed them one day (David Solomon will take the reins after Lloyd Blankfein's retirement.) Mentors come in all forms:

It is important to discover the people whose personalities, integrity and work ethic you admire and then place them on your team. It doesn't always have to be an explicit "will you be my mentor"/"will you be on my personal board." They know, and you know. Personal relationships are incredibly sacred and given constant effort to maintain & grow, can be incredibly valuable. Forbes

Fortune Google Images The Chronicle The Cut Wall Street Journal Investopedia |

RSS Feed

RSS Feed