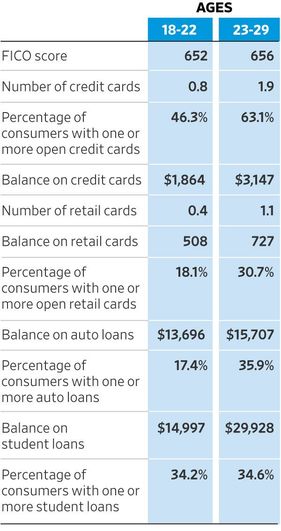

School is back in session! Now, guaranteed, college kiddos are far more concerned with Animal House like ragers at KA than which credit cards are going to help them down the road. But let's put these Natty Light and chicken-on-a-stick purchases to good use, shall we?! There was a great piece in the WSJ today titled Year-by-Year College Education in Credit Scores.  How can students use their four years at school to build a good credit rating and put themselves in a better position post graduation. Let's start with the stats above. A 22-year-old has a FICO credit score of 651 (the range is 300-850) on average and $2,012 in credit card debt. Generally as students get older and graduate, they open more credit cards and then rack up more debt as their lifestyles become more expensive and "adulting" begins.  So, let's break this down year-by-year with some tips on how to multi-task your partying, I mean studying, with building for your future. Freshman Year. Baby steps- parents can add their child as an authorized user on one of their credit cards. Warning to only do this if the parent themselves has a good credit score. If the parent doesn't, this could end up hurting your student from the start. Also, maybe have the talk of what justifies an "emergency" or else you could get some mass bar-tabs from Thirty Thursday. Oh wait, the drinking age is 21- never-mind! ;) The 2nd option which distances parent from child is a secured credit card. This card works essentially as a debit card as it is funded by depositing cash. The student would spend his/her money each month and then replenish it after paying the bill. 18 is the age at which students are able to begin requesting their credit score information. Using Experian or a similar credit bureau can help them understand how credit is built and why it is important.  Sophomore Year. Headed back for year 2! At this point- some kiddos might have a car by now- maybe not a Porsche like Elle Woods but making car payments on anything getting them across campus to that astronomy lab. Parents may be making the car payments while students pony up for gas- better for their credit score- flip this arrangement! If the student cosigns and makes said payments, it will help them down the road. However, most kids are focused on school and maybe don't have a part-time job so this burden could be too heavy. Evaluate your families personal situation and go from there! Paying cell phone or utility bills formerly haven't helped credit scores. However, students living off campus can now use Rental Kharma or ClearNow to have those payments reported to bureaus (albeit, make sure they are being paid in full and on time.) First unsecured credit card- try and gas or retail credit card the author says! Keep the balance low- never more than 30% of your credit line even if you're able to pay off more.  Junior Year. Classes getting a bit harder now, eh?! At this point- if students can make a small dent in that student debt, they will be money ahead. Even if more loans are going to be needed, any payments will be reported and can help credit scores. Keep trying to move forward with your credit cards as well. If you haven't graduated from your parents CC, try a secured CC, if you have a secured CC, try a retail or gas card. Retail or gas card? Try a full credit card from your bank.  Senior Year. Almost there! If you don't have a credit card at this point- definitely apply based upon your personal situation. Underwriting standards make it easier to get a card albeit the limit may be lower. If you have a card, try and negotiate for lower annual fees or APR. Although having a lower APR will save you money, the best way to save money is simple: be able to pay your bills every moth. It's not always possible for everyone and we recognize that. But life will be much easier if you don't start off with student loans AND credit card debt. Loans may be inevitable but daily spending is up to you.  The road after this is an exciting one. There will be peaks and valley's and sometimes being an adult is going to hit you hard but everyone has to grow up! There are ways to make your life easier or harder and keeping a level-head on your spending will surely ease your anxiety for the years to come.

Living in debt because of irresponsible spending or simply just not making cognizant efforts to stay in good financial standing will hurt your ability to provide for your family in the future. Everyone has a different situation and some are much more difficult than others. But really, don't make your life harder than it needs to be. Make a concerted effort to control your spending, borrow wisely all while enhancing your credit score will lead to a much nicer life. xx

0 Comments

Leave a Reply. |

RSS Feed

RSS Feed