Now that I have your attention... This post is not going to focus on my expertise in Bitcoin mainly because it is quite foreign to me. It is fascinating. Intriguing. A seemingly get-rich-quick scheme to nab a G550 one day. The Winklevoss twins are Bitcoin Billionaires...so why not you? On another note...sweet, sweet revenge, Mark Zuckerberg.

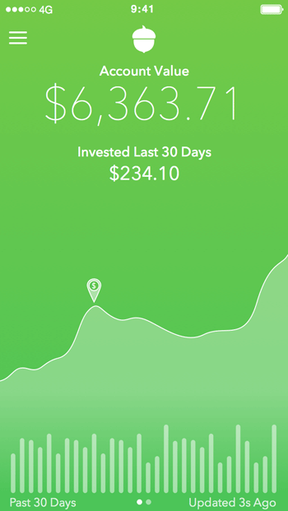

Before we delve into the excitement of Bitcoin, I want to run through some more...should we say, traditional ways of investing. These different platforms are tailored towards millennials who may not have large sums of money to invest.  Back "in the day," older generations called their broker to execute an order to buy a stock or bond. Word of which stocks were hot, were found in the newspaper, the workplace and spread by word of mouth. Today, you have the world at your fingertips. Within moments you can Google NYSE or NASDAQ followed by the ticker symbol and have a plethora of information. Once that information is garnered, you can head to your online broker, deposit money from your bank account and within a day or so, execute a trade and become a new shareholder. So how should you go about this? I discuss in Barneys, Bergdorfs & Bill$ that I use CapitalOne Sharebuilder. It functions like a normal online brokerage but there are now apps dedicated specifically to millennial investing. Let's check a few out...  In this week's edition of Barron's, the article "Scroll, Tap, Trade: Apps That Target Millennials" kicks off this discussion. Here are 3 apps the article discusses: Acorns. 2.5 million users. 70% are ages 18 to 34. $1/month.

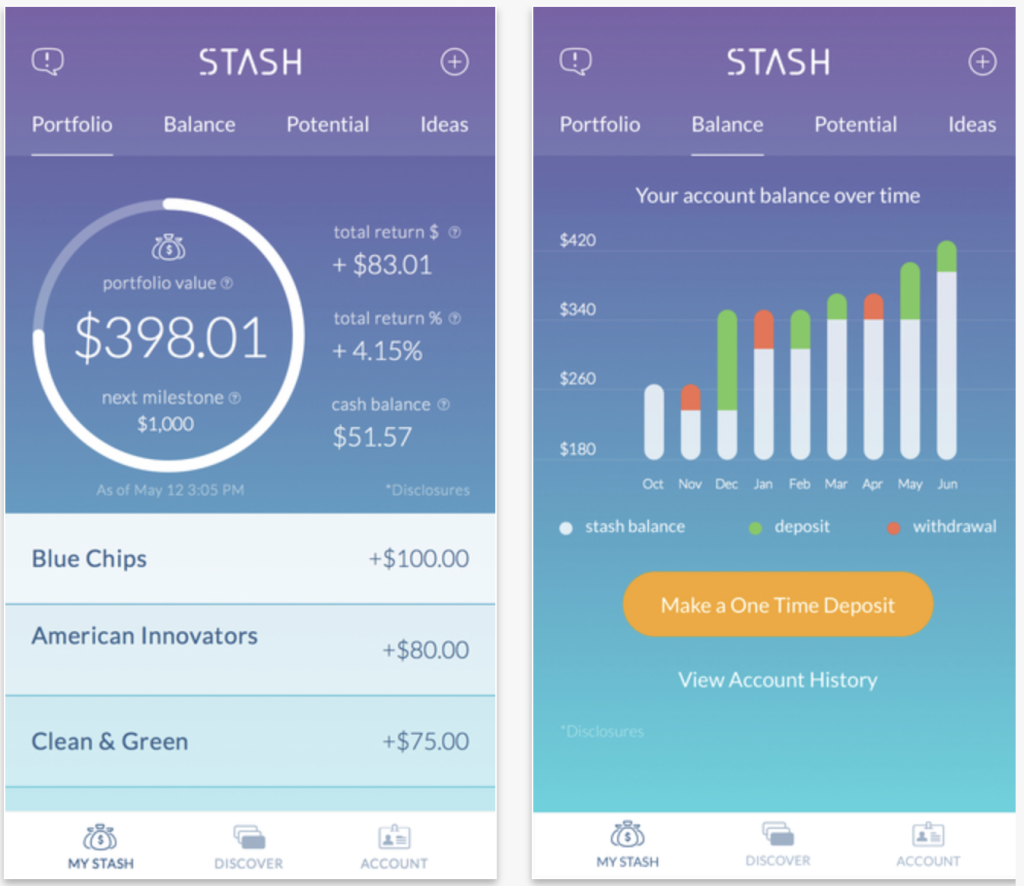

Stash. 1.5 million users. 66% are ages 18 to 34. $1/month. Began as strictly an investing platform and has now grown into retirement accounts with plans to "evolve" with their investors.

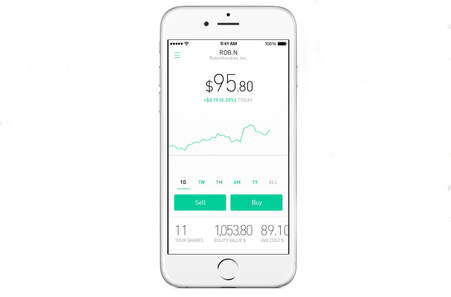

Robinhood. 3 million users. 77% under 36. No fees.

Now, as I have stated, I do not use these apps. I began my investing on CapitalOne and have simply kept my portfolio there so I do not have first hand knowledge of using these. From a glance, it appears these all basically do the same thing: make investing quick and simple. A big misconception with investing is you need to be rich starting out in order to jump in. Not the case. If you're having trouble making your monthly mortgage or car payments, then maybe this isn't the time as you don't want to drive up your debt obligations. However, you by no means have to be flush with cash. Putting in $100 or $200 is a fine way to start. An important thing to note are fees associated with investing. Either a monthly fee or a per trade fee will usually apply. Read the fine print!  Just from a bit of research, Stash looks to have a great "Learn" portion of their site. Their staff and contributors write articles on the principles of investing and other strategies. So what should you invest in? The stocks millennials overwhelmingly invest in probably wouldn't surprise you: Apple, Tesla and Snap (Snapchat) are a few. Warren Buffet talks about the investment strategy of buy what you use and know. Wear Nike? Buy Nike stock. Now, you will want to go about this with research as well. Just because you really love Under Armour's under shirts doesn't mean you should dive in head first (the company was the worst performer in the S&P 500 in 2017. But, hey, don't underestimate Kevin Plank...maybe it'll bounce back!)  The best and most important thing you can do is, well 1, do NOT invest money you don't have. Everyone has different risk tolerances, but taking out loans to jump into the stock market is generally not the way you way to start out. Also, do not neglect your current obligations. People have risked and struck it big but the ones who end up upside down in their debts outweigh those success stories. Besides that...RESEARCH. Read the newspaper. Watch CNBC. Subscribe to Barron's. If you are serious about investing and want to use the markets as a way to help fund a strong financial future, it is going to take some work. Unless you are trading day-in and day-out, you should think of your stock market plays as investments, not your income. Your day-to-day job is your income, this is a way to help give you some more cushion for the future. There is little substitution for good old fashioned hard work! Shortcuts have pitfalls.  It is not a sure thing. You've gotta risk it for the biscuit but keep in mind...you could lose it all. There are no guarantees when putting your money in a stock. The money you invest is not guaranteed to you. Putting your money in a bank is guaranteed you'll get it out. Funds are insured by the FDIC. Deposits up to $250,000 are safe by insurance. When you pick a stock, you're picking a company. You're picking it's culture, it's employees, executives and betting on its longevity. Now, there is a snowballs chance in hell Apple or GE won't be around in 25 years. But a good lesson (and obviously a very rare occurrence) was Enron in 2002. The stock price had soared, being propped up by falsified accounting practices. From 2001 to 2002, the stock price fell to $0 taking their shareholders down with them.  If something sounds too good to be true...it usually is. Bubbles are something to be aware of and leads us back into the topic of the fad of the year, Bitcoin. A bubble, from Investopedia, "occurs when investors put so much demand on a asset that they drive the price beyond any accurate or rational reflection of its actual worth. In the case of a stock, the actual worth would ideally be determined by the performance of the underlying company. Like the soap bubbles a child likes to blow, investing bubbles often appear as though they will rise forever, but since they are not formed from anything substantial, they eventually pop. And when they do, the money that was invested into them dissipates into the wind."  Now, I am not calling Bitcoin a bubble but there are massive parallel's with the cyrptocurrency to the definition above. From this week's edition of Barron's: "Here's one cyclical, but largely accurate, view of market cycles. Wall Street spots an exciting trend. Financiers fund companies and create financial products to play that trend. They get their pals, high-rollers, and insiders in early. Just as the trend starts to peak, the average Joe gets interested, and Joe's grandma too. Then the market crashes." If you have observed the rise of Bitcoin, you will know it is just the opposite. Bitcoin was invented in 2009. The now billionaire Winklevoss twins invested in April of 2013 when the cryptocurrency hit a high of $266. It now sits at $17,434 (12/12/2017; 12:01 PM EST.) Banks have not been at the forefront of this trend. Possibly the greatest example of this was JPMorgan Chase CEO, Jamie Dimon slamming it as a fraud at one of the most prestigious investor conferences of the year, Delivering Alpha.  Banks are now jumping on board to start offering the currency to their institutional investors. The CBOE (Chicago Board of Exchange) Futures Exchange began listing Bitcoin futures yesterday. This is a good sign because it lends legitimacy to the currency. The price of Bitcoin has been very volatile (moves up and down rapidly.) Bitcoin can fluctuate against fiat currencies because of its perceived value vs. the currency. Fiat currency is currency that a government has declared to be legal tender, but not backed by a physical commodity. The dollar used to be backed by gold (a physical commodity) known as the "Gold Standard". From 1971 on, it is no longer backed by gold, making the U.S. dollar a fiat currency. Fiat money is managed by governments that favor low inflation, high employment, and satisfactory growth through investment in capital resources. As a country's economy begins to show weakness, investors may move their assets into Bitcoin. When this has happened in the past, investors moved their money into gold. See the similarities?  This is all relevant to Bitcoin's volatility. Since fiat money is not "backed" by anything, it risks becoming worthless due to "hyperinflation." Hyperinflation basically causes a country's currency to be worthless. How? In countries like Zimbabwe and Venezuela, there has been a significant increase in the money supply but is NOT supported by gross domestic product (GDP) growth. Those two countries are in such disarray that when you receive a paycheck, because of hyperinflation, it might at well be Monopoly money! It's like making 100 widgets and no one wants to buy...if there is no demand, your supply is worthless. We are REALLY getting into the weeds here but I think it is important to understand how currencies work. The bottom line, and why proponents argue Bitcoin is far from a bubble is, like gold, there is a finite amount of the coins. 21 million BTC. Just as there is a finite amount of gold. This lends to both Bitcoin and gold's perceived "store of value." Countries can print infinite amounts of paper currency but gold and Bitcoin have a firm amount.  If you were reading this in hopes of tricks to get into Bitcoin and have your own Yacht A one day, I apologize for my lack of assistance! There have been bullish projections that the cryptocurrency could be worth $1,000,000/BTC by 2020. If it reaches that, there may be lots of people disappointed they didn't jump in, but as of now, I am not a Bitcoin investor. Mining of coins, cold storage (drives not connected to the Internet,) multiple copies of your Bitcoins stored in safes...all a bit too out of the box for me, but I do enjoy understanding it and I hope this made at least a little sense. If you have $17k to spare or want to try for a futures contract, go for it! For everyone else, I encourage you to take the step and look into Acorn, Stash, Robinhood, or any other platform that intrigues you to begin forming your portfolio. Go into investing eyes wide open and only invest what you're not afraid to lose. x, Sydney Investopedia. Stash. Acorn. Robinhood. Barron's. Dow Jones. Google Images.

2 Comments

Carson B

12/14/2017 11:31:02 am

This was so helpful! I’m glad to have gotten not typs, but a piece of mind from someone I know who has successfully invested! Thank you for a great read! Everyone’s finances are different as you stated :) xo Leave a Reply. |

RSS Feed

RSS Feed