|

"No one knew healthcare could be so complicated." Going to have to say that one is false. I think American's would be hard-pressed to find something MORE confusing than our healthcare system. Kudos to our new administration for trying to tackle the 800-pound gorilla first, but looking back, maybe something less complex would have been the better move. I don't know, something simple like tax reform... Young adults can probably relate to the processes of becoming an adult as a kind of "baptism by fire." From filing your taxes, to applying for jobs, to managing a full-time job rather than 12 hours of college classes a week, there are lots of firsts in this new time in our lives and many don't come with a manual.  The inspiration for this post is because I had one of these adulting moments arise yesterday. I returned home to get my mail and had an "Explanation of Benefits" from my healthcare provider, Anthem Blue Cross Blue Shield. With insurance, an annual physical is included with the premiums you pay as it is dubbed a routine yearly screening. For women, we also get other tests that are also covered annually. I did my physical in early July at a doctor I found on ZocDoc in NYC. I knew to ask if everything was going to be covered under this annual comped physical...their answer was yes. They also ran blood tests to test for a variety of things. SO, all should have gone well, right? A $400 physical bill and $2,000 from blood tests...I would have to say no.  So here are the unknown missteps of my experience to hopefully help someone in the future not end up with a massive bill. First of all is the basic task of deciding what you want to be responsible for paying AKA your deductible. The amount you pay monthly is your premium. This is the cost for having insurance whether you use it or not. When deciding your benefits (dental, eye, etc.) the higher your deductible, the lower your premiums. Your deductible is the amount you pay before your insurance kicks in. If you are fairly healthy and can absorb some doctors visits, choosing a high deductible will usually save you money in the end in terms of premiums.  Then comes co-pays. This is the amount you pay for going to see certain doctors (certain health plans don't have co-pay's.) Once again, if you're a hypochondriac and are at the doctor frequently, you would want to ensure you're paying extra in premium for a plan with no co-pay's to avoid a $50 fee every time you go to the doctor. For a general doctor visit, the cost is fairly low, maybe $25. When you go to specialists, eye, ear, nose & throat etc. the cost goes up. For urgent care and emergency rooms with our friends from Grey's, the cost for the co-pay is high but it is nothing like the bill that will come in the mail later. I explain all of this because I have both high deductible's and co-pays, hence why I was responsible for so much of this bill rather than my insurance stepping in. Questions TO ask. These are the absolute basics but I will leave you with what to ask for to ensure you are not stuck with a $2,000 bill also. When booking a new doctor, first of all make sure they accept your insurance carrier (Blue Cross Blue Shield, for instance.) If you are going in for things like an annual physical and they want to run tests, first ask if all of these are covered under the yearly physical you are granted with your insurance plan. I would also get it in writing. They ran crazy tests on me like an EKG which is completely excessive, hence the charges. If they are going to run blood tests, again, ask if they are covered. SECOND, doctors offices usually send this "lab work" out to a 3rd party. Although you may have checked that the doctor is "in-network" (takes your insurance) the lab might not be (as what happened with me.)  ^Real photo of me when trying to figure all of this out.

If this happens to you, know there IS room for negotiation usually. I got on the phone with Anthem and had them dispute the charges and ultimately ended up getting the labs covered at an "in-network" cost. This will only happen if you're actively paying attention to your bills and taking the time to make the call. xx, Sydney

0 Comments

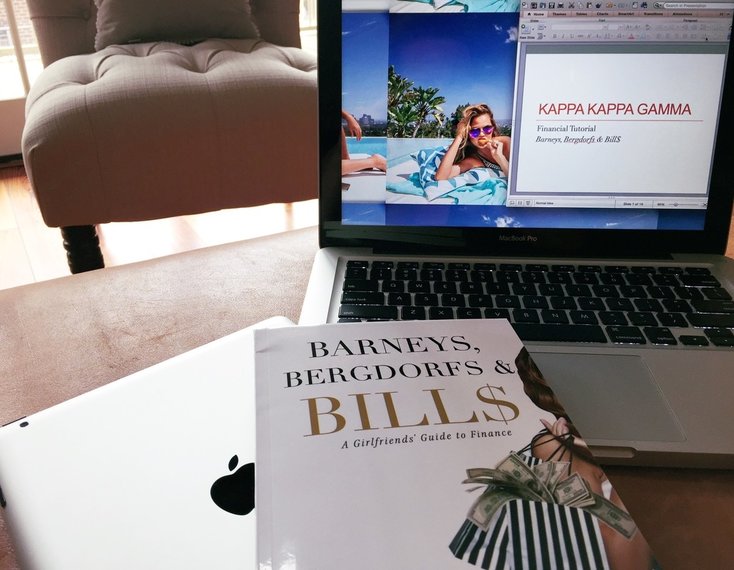

Coming out of college, I had a nonexistent credit score. Which I, of course, am incredibly thankful for. Not having to make regular student or car loans led me to have no credibility when it came to my ability to pay off a credit card. I had a debit card linked to my bank account but knew it was time to get my credit going. So I applied...for 3 cards...because I kept getting denied. I was probably quite lofty in my card expectations as I was applying for pretty high-flying cards with lots of perks...but the truth was, I could barely get a minimal card. I ended up with an American Express through our bank. American Express is great for their rewards. The card sufficed my needs but after having it for a year and consistently paying my bill on the exact day payment came due, I have established a good credit score and determined it was time to move on and, as Beyonce says, Upgrade U *to a new card.*  But how to choose? I am breaking down a few different cards to hopefully help streamline someone's hunt for the perfect card! To begin, let's start with the basics of credit cards and what sets them apart.

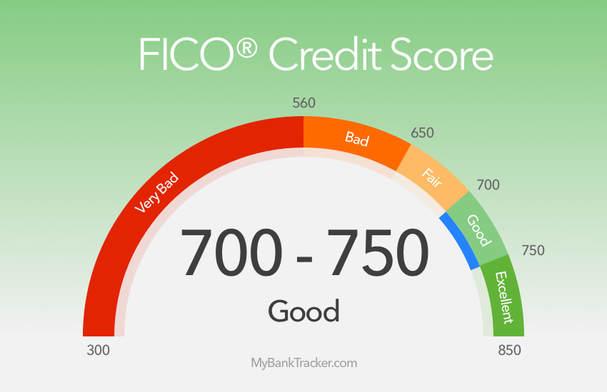

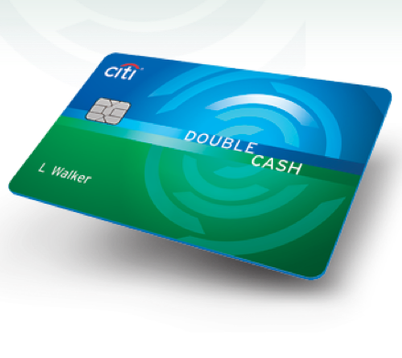

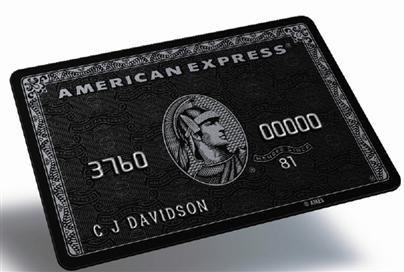

Bear in mind your credit score. You can check this for free on the FICO credit site. The more perks the card offers, the higher your credit score generally needs to be in order to obtain the card. Also keep in mind, applying for lots of cards WILL hurt your credit score. No/Low Credit  Capital One Quicksilver Cash Rewards Rewards: 1.5% cash back APR: 24.99% Annual Fee: $39 Minimum Credit: limited history The Overspender  Capital One Secured MasterCard -A secured card hedges your willpower. If you are worried you will overspend, hence destroying your credit score for years to come, stick with a secured card. Much like a debit card, you can only spend the amount you put up in collateral. APR: 24.99% Annual Fee: $0 Minimum Credit: no/low credit Cash Back  American Express Cash Back Rewards: 1-3% cash back (based on the purchase) APR: 13.99%-24.99% (based on credit score) Annual Fee: $0 Minimum Credit: Good (700-750)  Citi Double Cash Rewards: earn cash back twice, 1% on purchases, 1% when you pay for purchases APR: 14.49%-24.49% Annual Fee: $0 Minimum Credit: Good (700-750) Points, Points, Points  American Express Gold Card Rewards: 25,000 bonus points, 2-3x points/$1 APR:16.99%-23.99% Annual Fee: $0 first year, $195 after Minimum Credit: Good (700-750) World Traveler Chase Sapphire Preferred Chase Sapphire Reserve Rewards: 50,000 bonus points & 1-2 points/$1 Rewards: 50,000 bonus points & 3x points/$1 APR: 16.99%-23.99% APR: 16.99%-23.99% Annual Fee: $0 first year, $95 after Annual Fee: $450 Minimum Credit: Excellent (750-800) Minimum Credit: Excellent Why is the Reserve so expensive? Elite travel benefits and credits, higher point rewards for spending, unparalleled 24/7 customer service (a REAL human!) You can get a credit card for specific airlines: Delta, United etc. but with the Sapphire cards, the rewards are flexible, meaning you can redeem the points on different airlines not just one. Mack Daddy  American Express Centurion Black Card Rewards: numerous ranging from points, to VIP airport treatment, upgrades at hotels etc. Annual Fee: $7,500 initiation, $2,500 annual (invitation only, .1%) Annual Spending Requirement: $250,000 Minimum Credit: Excellent. Line of credit with LOTS of 0's required. Like mother, like daughter ;)  American Express

|

|  |

This borough map saved me when I first moved here. I highly recommend the website StreetEasy to find a sweet place. Using this map will help you narrow down your search results when you determine which neighborhood you want to live in. Look for No Fee places to save even more (that is the brokers fee which can be as much as 12-15% of the first years total rent.) A No Fee unit means you, as the renter, will not pay this fee. The landlord/owner of the unit will pay.

The other thing, you do NOT need a broker. I started with one and then using this site was able to find a place on my own, therefore eliminating that hefty cost. With a little, ok maybe a lot of, research you'll be good to go on your own, too.

The last thing is there are different "types" of places you'll see on this site. Apartments or Rental Units are the normal thing you would think of, probably the same deal as you had in college. There usually is no application process for these. Condominiums require an application and approval process. Usually there is an application fee and come with more paper work because the building's board must approve all tenants. Co-op's are similar in terms of the application process. If you're interested in a co-op or condo I would recommend starting the process sooner rather than later. Generally, in New York City, about one month out is when places come on the market so keep checking StreetEasy, contact the broker and get an appointment set up to see the unit as well as learn about what processes, deposits, reference letters etc. are needed.

Being able to prove you can pay the rent via your salary or a guarantor (your parents etc.) will also be something to investigate because getting that paper work can be a large task. Every building is different in how many times the rent you must be able to show (for instance you might have to prove you can show 20 times the rent so if you're paying $2,000/month, you need to be making at least $40,000.) The reason this is a big thing in NYC is because it is nearly impossible to evict someone. Renter laws are written to protect the tenant.

Moving anywhere new is stressful but choosing a huge city can amplify those worries. My advice: just do it. Start saving your bucks with Barneys, Bergdorfs & Bill$ so you can live how you want and just take a leap of faith and go for it. I'm big on risking it for the biscuit. You don't want to jump without looking but in my opinion, it's better than never jumping and simply being content. If you really want something, go get it!

The other thing, you do NOT need a broker. I started with one and then using this site was able to find a place on my own, therefore eliminating that hefty cost. With a little, ok maybe a lot of, research you'll be good to go on your own, too.

The last thing is there are different "types" of places you'll see on this site. Apartments or Rental Units are the normal thing you would think of, probably the same deal as you had in college. There usually is no application process for these. Condominiums require an application and approval process. Usually there is an application fee and come with more paper work because the building's board must approve all tenants. Co-op's are similar in terms of the application process. If you're interested in a co-op or condo I would recommend starting the process sooner rather than later. Generally, in New York City, about one month out is when places come on the market so keep checking StreetEasy, contact the broker and get an appointment set up to see the unit as well as learn about what processes, deposits, reference letters etc. are needed.

Being able to prove you can pay the rent via your salary or a guarantor (your parents etc.) will also be something to investigate because getting that paper work can be a large task. Every building is different in how many times the rent you must be able to show (for instance you might have to prove you can show 20 times the rent so if you're paying $2,000/month, you need to be making at least $40,000.) The reason this is a big thing in NYC is because it is nearly impossible to evict someone. Renter laws are written to protect the tenant.

Moving anywhere new is stressful but choosing a huge city can amplify those worries. My advice: just do it. Start saving your bucks with Barneys, Bergdorfs & Bill$ so you can live how you want and just take a leap of faith and go for it. I'm big on risking it for the biscuit. You don't want to jump without looking but in my opinion, it's better than never jumping and simply being content. If you really want something, go get it!

http://blogs.wsj.com/economics/2016/03/10/the-most-expensive-cities-in-the-world-to-live/

http://coolspotters.com/characters/serena-van-der-woodsen/and/accessories/louis-vuitton-ipad-case#medium-878766

http://www.businessinsider.com/view-from-top-of-432-park-avenue-2014-10

http://www.nyctourist.com/map1.htm

http://coolspotters.com/characters/serena-van-der-woodsen/and/accessories/louis-vuitton-ipad-case#medium-878766

http://www.businessinsider.com/view-from-top-of-432-park-avenue-2014-10

http://www.nyctourist.com/map1.htm

Whenever I get a paycheck for a large amount, it seems like it will last me forever. Then I go to the grocery store. And CVS. And out to dinner. And then accidentally stop in at Bergdorf Goodman and buy a new purse. Whatever, that's off topic. Pretty soon, that paycheck is dwindling down to the nubs. Has a dollar always only been 100 cents? I swear my parents credit card used to get me a lot further ;)

So how do you 1) keep that paycheck tighter to the vest and 2) maybe even, dare I say, make some money off of it? Oh yeah, I'm talkin' investments. Real adulting going on right here.

There are a few options but the good thing about all of these is that your money is not going to be accessible to you, therefore the temptation of a new handbag will be out of the picture.

If you want to just start easy, the best way to keep your paws off your cash and make some money is to put your cash in a savings account. Now, currently we live in a world of incredibly low interest rates (even negative rates in some cases.) Basically, when your money sits in a checking account, it makes no interest because that money is readily accessible to you. The reason why you "make" money when your cash sits in a savings account is because you are allowing others to borrow. It's not as blatant as your bank saying "hey, can we lend your money out to Jim since you don't need it right now?" But that basically is what happens.

Also, just like lending money to a friend, you're probably thinking "well, what if they don't pay my money back to the bank." No worries there either. All of your accounts up to $250,000 are insured by the FDIC (Federal Deposit Insurance Corporation.)

Something a little more advanced than just transferring money from your checking to savings is getting into the stock and bond market. Now, the bond market is more complex to detail in this post but essentially, you make money on a bond via an interest rate as well. In the stock market, you can make money 2 ways: a capital gain and dividends (if you're interested in more on bonds check out the book as it is all detailed.)

Capital Gain. This is the main money maker people think about when pondering the stock market. Let's say you bought 10 shares of a publicly traded company, Apple for instance. Apple (AAPL) trades currently at about $116 a share on the NASDAQ (a stock exchange), so these 10 shares cost you $1,160. Let's assume in 1 year, Apple's stock price is now $135 and you decide to sell for a total of $1,350. You would have a capital gain of $190. You also need to consider the chance the stock price could go down, leaving you with a capital loss.

Dividends. These are not offered on all stocks. A dividend is a sum of money paid to company stockholders (usually quarterly.) For example, in April, Apple had a dividend of $.57/per share. In order to show this, we will assume we own 100 shares. Each quarter (4 times a year,) for as long as you are an owner of the stock, you will be paid $.57/share, which is $57. That doesn't seem like much in the grand scheme of things but with the more shares of a stock you own, the more you will be paid.

This is just wading into the world of investments and I'm sure some of you are looking at this post with a face similar to Nicki's. It can be frustrating to watch your bank account just get lower and lower and this may seem confusing. However, by starting to think about tucking some of your earnings away either just in the form of savings or getting into investing, you will be setting yourself up for a more financially successful future.

So how do you 1) keep that paycheck tighter to the vest and 2) maybe even, dare I say, make some money off of it? Oh yeah, I'm talkin' investments. Real adulting going on right here.

There are a few options but the good thing about all of these is that your money is not going to be accessible to you, therefore the temptation of a new handbag will be out of the picture.

If you want to just start easy, the best way to keep your paws off your cash and make some money is to put your cash in a savings account. Now, currently we live in a world of incredibly low interest rates (even negative rates in some cases.) Basically, when your money sits in a checking account, it makes no interest because that money is readily accessible to you. The reason why you "make" money when your cash sits in a savings account is because you are allowing others to borrow. It's not as blatant as your bank saying "hey, can we lend your money out to Jim since you don't need it right now?" But that basically is what happens.

Also, just like lending money to a friend, you're probably thinking "well, what if they don't pay my money back to the bank." No worries there either. All of your accounts up to $250,000 are insured by the FDIC (Federal Deposit Insurance Corporation.)

Something a little more advanced than just transferring money from your checking to savings is getting into the stock and bond market. Now, the bond market is more complex to detail in this post but essentially, you make money on a bond via an interest rate as well. In the stock market, you can make money 2 ways: a capital gain and dividends (if you're interested in more on bonds check out the book as it is all detailed.)

Capital Gain. This is the main money maker people think about when pondering the stock market. Let's say you bought 10 shares of a publicly traded company, Apple for instance. Apple (AAPL) trades currently at about $116 a share on the NASDAQ (a stock exchange), so these 10 shares cost you $1,160. Let's assume in 1 year, Apple's stock price is now $135 and you decide to sell for a total of $1,350. You would have a capital gain of $190. You also need to consider the chance the stock price could go down, leaving you with a capital loss.

Dividends. These are not offered on all stocks. A dividend is a sum of money paid to company stockholders (usually quarterly.) For example, in April, Apple had a dividend of $.57/per share. In order to show this, we will assume we own 100 shares. Each quarter (4 times a year,) for as long as you are an owner of the stock, you will be paid $.57/share, which is $57. That doesn't seem like much in the grand scheme of things but with the more shares of a stock you own, the more you will be paid.

This is just wading into the world of investments and I'm sure some of you are looking at this post with a face similar to Nicki's. It can be frustrating to watch your bank account just get lower and lower and this may seem confusing. However, by starting to think about tucking some of your earnings away either just in the form of savings or getting into investing, you will be setting yourself up for a more financially successful future.

Ugh, politics. I love it. But currently hate it. This post is not to tell you who to vote for. This is not about Donald Trump or Hillary Clinton but on the other elections happening this year that have been dwarfed in importance because of the media circus surrounding our presidential candidates.

I am writing this to inform on the other races taking place because 1) it is the last day to register to vote in some states 2) the "other" races have not been as widely talked about and 3) they are a little more complex and a large percentage of American's are uninformed on their importance. I'm talkin' about Congress. There really should be a "Girlfriends' Guide to Politics"...

Congress is divided into 2 parts: the House of Representatives (which I will refer to as the House) and and the Senate.

I am writing this to inform on the other races taking place because 1) it is the last day to register to vote in some states 2) the "other" races have not been as widely talked about and 3) they are a little more complex and a large percentage of American's are uninformed on their importance. I'm talkin' about Congress. There really should be a "Girlfriends' Guide to Politics"...

Congress is divided into 2 parts: the House of Representatives (which I will refer to as the House) and and the Senate.

This year, in the 2016 election, Senate seats in 34 states, and all 435 House seats are up for election. Elections will determine which party is the minority and the majority. Currently both the House and the Senate, so Congress, is controlled by the Republican party. Therefore the majority leaders of both the House and the Senate are Republicans and the minority leaders are Democrats.

House of Representatives. The number of seats (a total of 435) is determined by state population. That means the state of California obviously has more seats than Wyoming. 246 seats are currently occupied by Republicans to the 186 by Democrats. The head of the House, known as Speaker of the House, is Paul Ryan (R-WI.) The majority leader is Kevin McCarthy (R-CA.) Minority leader is Nancy Pelosi (D-CA.)

Senate. The number of seats in the Senate is different from the House as it is not determined by population. Each state has two representatives no matter their population. Some states, for instance Alabama, have 2 Republican senators. States like Colorado have 1 Republican and 1 Democrat. 54 seats are currently occupied by Republicans to 46 by Democrats. The head of the Senate is the Vice President, who is of course, Joe Biden (D.) The majority leader is Mitch McConnell (R-KY.) Minority leader is Harry Reid (D-NV.)

Let's throw it back to high school (maybe middle school) civics. There are 3 branches of government. The Executive branch is the President of the United States (POTUS) as well as a couple million employees. The Judicial branch is made up of the courts (Supreme Court and lower.) The final is the Legislative branch which is, of course, the House and the Senate. They meet in that building in the top photo located in Washington D.C., the Capitol building in the area known as Capitol Hill.

Legislative means lawmaking which is exactly what Congress does. It shares those powers with POTUS and the Supreme Court. So while we are electing ONE person (very powerful, nonetheless) to be president, this year we are also electing FOUR HUNDRED AND SIXTY NINE members of Congress on November 8, 2016. How many times have you heard about this on the news? Not many I would venture to guess.

The bottom line to this post is I know people are completely fed up with this election. I have heard "I'm not voting. I don't like either of them" SO many times. I am writing this to say DO NOT NOT VOTE. There is far more at stake, no matter if you are a Democrat or Republican, than just who becomes president. Although the president is a more public figure as compared to the members of Congress, these people are the ones that work with them to get bills passed and laws changed, made or enforced in this country. Lot's of these effect your $$$...so I would pay close attention.

You need to vote. It is your duty as an American citizen. Whoever you choose, do your research and make an informed decision and walk out of that polling station (or after you mail that absentee) feeling super proud to be an American.

Full radio interview:

http://www.supertalk.fm/archives/audio-archives/gallo-archives/?recording_id=19872

www.270towin.com

www.senate.gov

www.storify.com

www.politicspa.com

RSS Feed

RSS Feed